Livorno is Italy’s third largest commercial port – after Trieste and Genoa. Trade has flowed through its docks for hundreds of years, from a long-established fishing industry to newer cruise ships carrying thousands of tourists. Yet a new industry may be arriving at the city’s doorstep.

A potential gas pipeline linking Livorno with a liquefied natural gas (LNG) terminal in Barcelona is being heralded by its supporters as a potential route for LNG initially imported into Spain to reach the wider European market. It would be the highest capacity pipeline in Europe, capable of transporting 17 billion cubic metres of gas.

A ‘virtual’ gas pipeline is also being proposed, making use of a Floating Storage Regasification Unit (FSRU) – a large boat which stores LNG before it is transferred to the mainland – already anchored outside Livorno. Both the Spanish and Italian companies responsible for gas infrastructure (Enagas in Spain and Snam in Italy) have signed a Memorandum of Understanding on the pipeline, with feasibility studies being carried out.

This is far from the only fossil gas project proposed in response to Europe’s energy crisis. Similar FSRUs are also planned in Italy. Snam have purchased an FSRU anchored in Piombino capable of storing 5 billion cubic metres of LNG and a similar boat is being acquired for Ravenna on the Adriatic coast.

The proposal to route a gas pipeline from Spain to Italy is also in part an attempt to pressure France into backing the MidCat gas pipeline – a previously mothballed third connection between France and Spain’s gas networks. The pipeline was first proposed over a decade ago, and a 90km section has already been built in Catalonia.

Construction came to a standstill in January 2019 when the Spanish and French energy regulators rejected a request for additional investment by Enagás and Teréga – the two main promoters. Regulators pulled the plug after concluding that MidCat would increase energy bills and that the costs would outway the benefits for consumers.

The attempt to resurrect MidCat has not gone unnoticed however. Catalans have reformed the Plataforma Resposta al MidCat platform, which was ultimately successful in stopping construction of the pipeline in 2019. However, German Chancellor Olaf Scholz recently declared his support for MidCat, and a Spanish-German summit will start on Wednesday (5 October).

Europe was already moving towards renewables to combat the climate emergency before the energy crisis kicked in. It is not possible to switch focus back to new gas infrastructure now while honouring the EU’s climate objectives, and would not be sensible either. It will be years before any new gas projects receiving the green-light today become operational, and Europe is already able to meet its most important energy needs for the upcoming winters.

This new splurge in fossil gas spending is being enabled by the European Commission’s REPowerEU plan. In theory, the plan aims to switch Europe to more reliable energy sources and to eventually end its dependence on Russian fossil fuel imports after its hostile invasion of Ukraine.

The EU currently imports the vast majority of fossil fuels it uses from outside the bloc. Over 40 percent of its imported gas, 46 percent of imported coal and 27 percent of imported oil come from Russia.

Breaking this dependence is no trivial matter, yet RePowerEU goes even further. It rewrites the EU’s role in an already rapidly changing world, starting with energy.

REPowerEU does this by sidelining other EU policies such as the European Green Deal or the ‘Fit for 55’ plan to transition to a greener economy. It diverts funding from the NextGenerationEU pandemic recovery fund to support a total rush for gas projects like the pipeline connecting Livorno and Barcelona. The goalposts have moved – what were once plans to green Europe’s energy system have switched primarily to securing it at increasing cost to the environment.

On top of the promised €245 billion made available from the European Green Deal, Fit for 55 package and NextGenerationEU, REPowerEU dangerously proposes to use almost €40 billion from other existing public funding streams and measures at EU level. All of these instruments could be mobilised to finance new renewable energy to reduce dependence on Russia – or damaging fossil fuel infrastructure accelerating the climate crisis.

It will be years before any gas travels through a pipeline between Livorno and Barcelona – if any ever does – yet the risk of a construction boom locking Europe into burning gas for decades is very real. European taxpayers would be paying for this lock-in, the same taxpayers currently struggling to pay their energy bills. EU institutions continue to pitch new gas infrastructure as a long-term, sustainable option. We are afraid that it is not.

Authors:

Josep Nualart Corpas is Climate and Energy Researcher at Catalan NGO Observatori del Deute en la Globalització (ODG).

Elena Gerebizza is Energy and Infrastructure Campaigner at Italian NGO ReCommon.

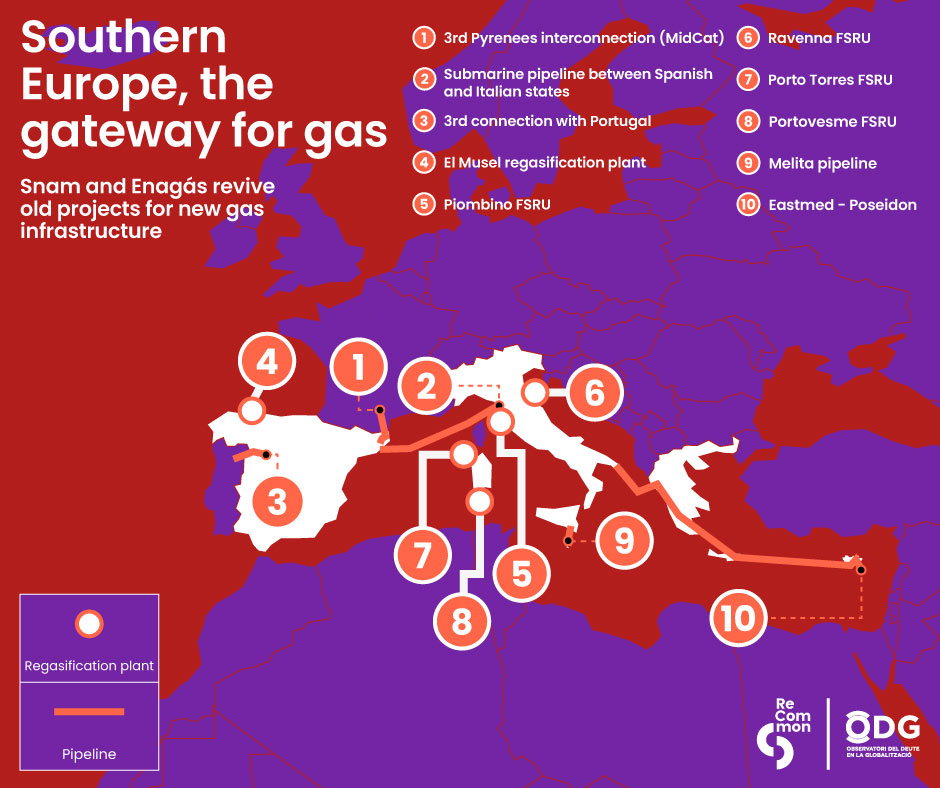

Information about connections in the map

1 | 3rd Pyrenees interconection (MidCat)

Location: Hostalric (Spanish state) – Barbaira (France)

Proponent/ Gas TSO or other company: Enagás & Teréga

Capacity: 9 bcm

Investment Spanish part: Public; 370M€ (225M€ in 2022-2026 and 145M€ in 2027-2030).

Investment mechanism: REPowerEU / Next Generation EU

Where the gas will come from? : Algeria (through pipeline) or LNG imported from USA, Russia, Nigeria and Qatar (through Cartagena, Sagunto and/or Barcelona’s regasification plants)

Construction: to be completed between 2025 and 2029 (depends on the source)

2 | Submarine pipeline between Spanish and Italian states

Location: Barcelona (Spanish State) – Livorno (Italy)

Proponent/ Gas TSO or other company: Enagás & Snam

Capacity: 15-30bcm

Investment Spanish part: Public; 1.500M€ (365M€ in 2022-2026 and 1.135M€ in 2027-2030)

Investment mechanism: REPowerEU / Next Generation EU

Where the gas will come from?: Algeria (through pipeline) or LNG imported from USA, Russia, Nigeria and Qatar (through Cartagena, Sagunto and/or Barcelona’s regasification plants)

Construction: to be completed in 2028

3 | 3rd conection with Portugal

Location: Celorico da Beira (Portugal) – Zamora/Adradas (Spanish State)

Proponent/ Gas TSO or other company: Enagás & REN Gasodutos

Capacity: 2.6 bcm (up to 5.2 bcm)

Investment Spanish part: Public; 110M€ (90M€ in 2022-2026 and 20M€ in 2027-2030).

Investment mechanism: REPowerEU / Next Generation EU

Where the gas will come from?: Not available

Construction: Not available year of construction

4 | El Musel regasification plant

Location: Xixón/Gijón (Spanish state)

Proponent/ Gas TSO or other company: Enagás

Capacity: 7 bcm. Only for bunkering. It is ilegal as a regasification plant and have changed its purpose to “logistic infrastructure” for bunkering and LNG storage

Investment: 318.7 M€ – 282.8 M€ paid through the gas bill from 2012 to 2023.

Investment mechanism: Regulated return

Where the gas will come from?: Not available

Construction: Completed, start operation in 2023

5 | Piombino FSRU

Location: Port of Piombino (Livorno)

Proponent/ Gas TSO or other company: Snam Spa

Capacity: rigassification 5 bcm per year; storage 170,000 cm

Investment: 330M€ (purchase Golar Tundra)

Investment mechanism: regulated return

Where the gas will come from? Not available

Construction: operational in spring 2023

6 | Ravenna FSRU

Location: Ravenna offshore

Proponent/ Gas TSO or other company: Snam Spa

Capacity: regassification 5 bcm per year; storage 170,000 cm

Investment: 400M€ (purchase of BW Singapore)

Investment mechanism: regulated return

Where the gas will come from? Not available

Construction: to be completed in 2024

7 | Porto Torres FSRU

Location: Porto Torres (Sassari)

Proponent/ Gas TSO or other company: Snam Spa

Capacity: regassification not available; storage 25,000 cm

Investment: not available

Investment mechanism: regulated return

Where the gas will come from?: Not available

Construction: to be completed in 2025

8 | Portovesme FSRU

Location: Portovesme (Carbonia-Iglesias)

Proponent/ Gas TSO or other company: Snam Spa

Capacity: Regassification: 3,5 bcm per year; storage 140,000 cm

Investment: 269 M€ (purchase Golar Arctic); conversion into FSRU

Investment mechanism: regulated return

Where the gas will come from? Not available

Construction: to be completed by mid 2024

9 | Melita pipeline

Location: Gela (Sicily) – Marsaxlokk/ Delimara (Malta)

Proponent: Melita Trans Gas Company Ltd, Snam Spa

Capacity: 2 bcm per year

Investment: 211M€

Investment mechanism: TEN E, Connecting Europe Facility (feasibility studies)

Where the gas will come from?: Exported from Italy to Malta

Construction: to be completed in 2024

10 | Eastmed- Poseidon

Location: Israel (offshore) – Cyprus – Greece (including Crete) – Italy

Proponent: IGI Poseidon SA (50% Depa International Projects, 50% Edison)

Capacity: 11 bcm per year (up to 20 bcm)

Investment: 6B€ (estimated)

Investment mechanism: CEF funding (tbc), investment decision by end of 2022

Where the gas will come from?: Israel, Cyprus

Construction: to be constructed and operational by 2027